BURNABY, A.

DUTY ON MALT OR ALE?

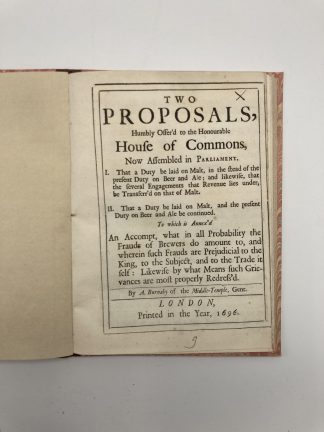

Two Proposals humbly offer’d to the Honourable House of Commons Now Assembled in Parliament.

London, n.pr., 1696£1,250.00

FIRST EDITION. pp. [ii], 26:[]1, A-C4, D1. Roman letter some Italic. Title within double ruled border. Small burn hole to two leaves affecting a couple of letters, cut a little close at fore-edge margin. A very good copy in modern calf-backed marbled boards, spine with raised bands ruled in gilt, red morocco label gilt.

Rare first edition of this interesting work on taxation, proposing a tax on Malt rather than on Beer as a means of ensuring social justice within the tax system. Tax on beer and malt were most important in terms of revenue for the Crown:“The yield on these two taxes was one of the Pillars upon which the public finances fo the country rested.” Peter Mathias. “By far a majority of the writers (of the end of the seventeenth century) believed that the excise rested on the mass of consumers in general, irrespective of the fact whether they were poor or rich. This broad theory was ushered in by the famous economist and statistician, Sir William Petty. Petty also has the distinction of being the first English writer to devote an entire work to the subject of taxation… The views of Petty gradually diffused themselves throughout the community, keeping pace with the ever-widening use of indirect taxes on consumption. Many of the writers of the close of the seventeenth century now became ardent advocates of the general excise.The same belief in the excise, on the score of its reaching the entire mass of the consumers, is found in the work of Burnaby, who advocated an extension of some of the internal duties on commodities. His particular scheme was the imposition of a tax on malt, which in his opinion “will be less felt than usually Taxes are, by reason every Person will pay Proportionable in the Price of Malt.” He lays down his general principle as follows: “The more universal any Tax is, it is to be supposed (unless in some Particular Cases) to be the more equal.” Then follows the minor premise: “I presume, no Person will deny that such a Tax will prove so universal, that not any Person will escape paying his Proportion according to his consumption.” From all of which it is easy to draw the conclusion that “no Person can complain; who Consumes little, will have but little to pay.”” Seligman. ‘The shifting and Incidence of Taxation’.

The work offers much insight in the brewing practises of private family and small brewers and the trade in beer and spirits generally. Burnaby proposes eight ways in which the taxing of malt rather than beer will be preferable to the tax collector (simplicity, equality, efficiency, the reduction of fraud etc.) and then offers examples of what might cause objections to his ideas, followed by his refutation of these objections. A rare and most interesting work.

Wing B.5742. Goldsmiths\\\\\\\' 3258. Kress 1940.In stock